Download Visual Summary of Housing Stats for Western Region

Housing cost and availability continue to be amongst the key challenges facing the Irish economy and Irish society. In the Western Region, as elsewhere, the impacts are significant and include the stifling of economic development and investment, the creation of regional and intra-regional imbalances and increased levels of youth displacement and emigration. There are also impacts on people’s well-being and choices at key life stages and at a wider societal level, on social cohesion and on the capacity to build balanced communities, particularly in areas of high demand.

Housing issues in the Western Region reflect broader national issues but are intensified by particular regional challenges. These include limited investment in the kind of infrastructure which supports housing development, including water, sewage and the electricity grid; the dominance of tourist-oriented housing stock in some areas; and the financial viability of construction for developers where costs can exceed the market value. This blogpost highlights some pertinent recent Western Region statistics and patterns in areas such house and rental prices but also in housing completions, commencements and planning permissions. The latter are important indicators of what we can expect in terms of housing supply in the region in the medium to longer term.

House Prices

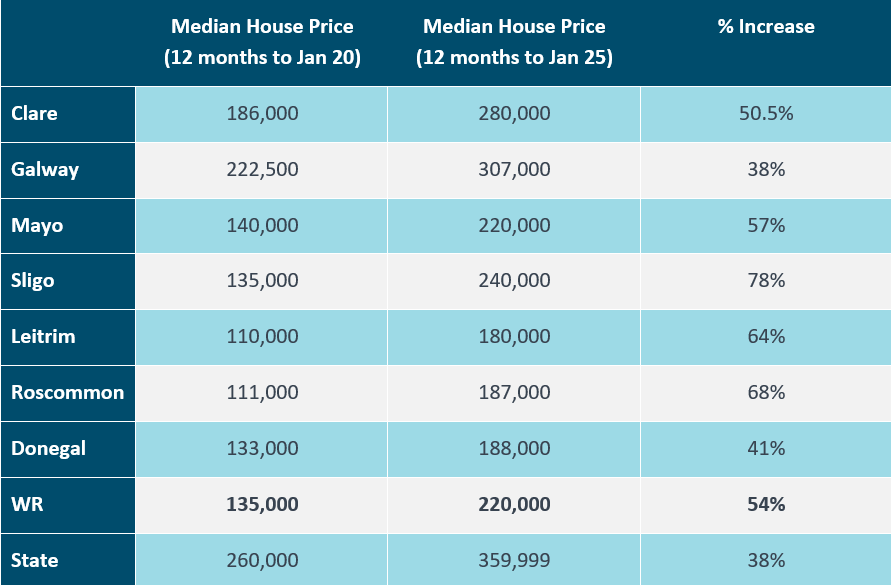

Whilst house prices in the Western Region overall remain amongst the lowest in the State, they have in the last five years increased substantially – and at a significantly higher rate than in the remainder of the State. As Table 1 shows, median house prices in the region overall increased by 54% in just the last five years (between the 12 months to January 2020 and the 12 months to January 2025). This compares to a figure for the State overall of 38%. Only Galway at 38% is at a similar level to the State average but that is accounted for by its relatively high median house prices in 2020 as now: €222,500 in 2020, compared to €186,00 in Clare (the next highest) and €110,00 in Leitrim (the lowest in the region).

Sligo experienced by far the highest growth in median house prices in the region over the five-year period at 78%, followed by Roscommon at 68%, Leitrim at 64%, Mayo at 57%, Clare at 50.5%, Donegal at 41% and Galway at 38%.

In the 12 months to January 2025, Leitrim remains the county in the region – and the country – with the lowest median house price of €180,000. The next lowest median house price in the region is in Roscommon (€187, 000) and then Donegal (€188,000). There is then a notable gap between these three counties and what we can describe as the next ‘set’ of counties – Mayo at €220,000, Sligo at €240,000 and Clare at €280,000 with Galway, at €307,000 having the highest median house price by early 2025.

Table 1: Median Property Prices Western Region & State, 12 months to Jan 2020 to 12 months to January 2025.

Source: CSO, Residential Property Price Index

These patterns of significant increases in house prices both nationally and regionally show little signs of abatement. In the year from January 2024 to January 2025, average house prices rose nationally by 8.5%. Again, the Western Region recorded higher than average increases. The NUTS 3 Border Region (which includes Sligo, Leitrim and Donegal) recorded the highest increase nationally at 12.5% while in the West Region (comprising Galway, Mayo and Roscommon) prices increased by 10.8% (CSO, Residential Property Price Index).

Residential Rents

Similar patterns can be found when we look at residential rents. In the last five years, the increase in the cost of renting in the region has been phenomenal. Research from daft.ie published early in 2025[1] found that rents have increased by an average of 79% across the Western Region since before Covid (i.e. 2020), with especially high increases in Leitrim (98%), Roscommon (91%), Donegal (83%) and Mayo (81%). Leitrim and Roscommon had in fact the largest increases in the State in that time period with only Limerick City, Cavan and Longford outside of the region also experiencing growth rates of 80% plus.

As can be seen from Table 2, this pattern of particularly high rental cost increases has continued: the year-on-year increase to Q3 2024 on existing tenancies was 4.7% nationally but was 7.9% in the Western Region. Again, Galway recorded the lowest increase at 4.1% but all other counties experienced an increase well above the State average: Leitrim at 6.5%, Sligo at 6.9%, Clare and Mayo both at 7.8%, Roscommon at 8.6% and Donegal the highest in both the region and country at 13.7%, nearly three times the national average.

Year-on-year rent increases in new tenancies were, as expected, higher still: 6.4% on average in the State and 9.95% in the Western Region to Q3 2024. In this case, it was Leitrim which experienced the highest increase – a massive 25% in just one year while curiously, Donegal only experienced a 3.5% increase. Roscommon was also just under the State average at 4.9% but all other Western Region counties were above as can be seen in Table 2 below. At the time of writing (June 2025), the Government has just announced major reforms to the rental sector[2], which includes the extension of rent controls to the whole country. In time, such measures should curb the currently very high level of year-on-year increases in the rental sector in the Region.

Notwithstanding these increases, residential rents in the Western Region largely remain well below the State average. The average monthly rent in the Western Region (Q3 2024) for existing tenancies stood at 70% of the State average – €934 compared to €1334 in the State overall. For new tenancies, the comparable figure was 71% – an average of €1172 in the Western Region versus €1658 in the State. Galway is once again the outlier. The average rent in an existing tenancy in Q3 2024 was €1287, not far below the State average and a full €344 per month higher than the next most expensive county (Clare where the average was €943) and €523 higher a month than in Leitrim, the cheapest at €764 a month. Put another way, it costs an average of over €6000 more to rent a property in Galway for a year than it does in Leitrim.

Table 2: Average Monthly Rents and Year-On-Year Increases, Q 3, 2024, Western Region & State.

Source: Residential Tenancies Board, Rent Index Report Q3 2024

Linked to this is of course the lack of availability of properties for rent. With the proviso that it is only one source and that many rentals happen via word of mouth, family and community connections and other means, a snapshot of availability of properties for rent via Daft.ie presents a startling picture of under-supply. On the morning of the 12th of June 2025, there were 189 properties listed for rent in the entire seven county region. Galway City and County combined had the greatest availability at 93 – itself very low in the context of the size of the population, the economic vitality of the city and the presence of large third-level institutions – but no other county had more than 25 properties available. Leitrim had only six properties for rent and Sligo only ten.

The Pipeline: New House Completions, Commencements & Planning Permissions.

Housing Completions

A previous WDC Insights blogpost on 25 years of change in housing patterns available here, highlighted the steep decline in housing completions in the Western Region over 25 years and the virtual collapse in the years following the economic downturn post 2008 period. Western Region counties combined had 10,332 new house completions in 1999, or 22% of State total. Contrast this with 2014, for example, where there were only 1,071 new house completions in the whole region, just over 10% of the number built 15 years earlier. It would be 2018 before the numbers of completions in the region exceeded 2000 again and the figure for that year was only 2039 (CSO). To some extent this reflects the Celtic Tiger legacy of comparatively high levels of regional housing stock relative to population, levels of oversupply and persistently high vacancy rates. It meant that for a period, the Western Region had a comparatively high capacity to accommodate population growth without significant new construction, albeit with some intra-regional variation.

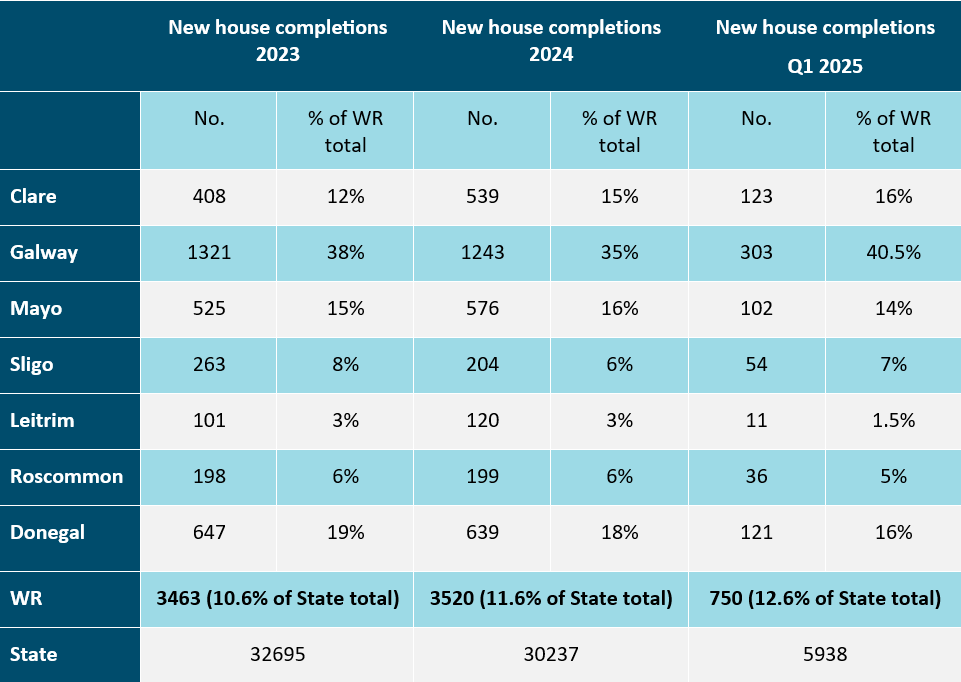

However patterns in the last five years in particular – the rise in regional housing demand, a clear shortage of suitable regional housing stock, and steep increases in house prices and rental prices as we have noted above – indicate that this capacity has now clearly been absorbed. The population of the region grew by 6.5% between Census 2016 and 2022, a larger increase than that of the housing stock at 4.2% (CSO). A key driver of this population growth has been net migration, i.e. people moving to the region from elsewhere, which will have had a particular impact on housing demand. Census 2022 shows that, in five of the seven Western Region counties (Clare, Leitrim, Mayo, Roscommon, and Sligo), more people moved in than were added through natural population increase. For example, Leitrim’s population grew by 3,043 people (9.5%) between 2016 and 2022. Of this, 2,254 (around 75%) was due to net migration. Yet during that same period (Q1 2016 to Q1 2022), only 366 new houses were completed in the county (CSO). More generally, we can say that although the numbers of house completions in the region has moved steadily upwards in the last number of years – rising to 2824 in 2020, 2753 in 2021, 3484 in 2022, 3463 in 2023 and 3520 in 2024 (CSO) – it is clearly not enough to meet current or projected future demand.

When we consider that the region accounts for national 17.2% of the population of the State, (Census 2022) we can see also see from Table 3 that it now also has a lower than might be expected share of national housing completions. In 2023, the 3463 completions represented 10.6% of the State total. This rose to 11.6% in 2024 and for Q1 2025, stood at 12.6% of the national figure. This small but steady increase is welcome but clearly a substantial increase in house completions in the region both in absolute numbers and relative to the rest of the country is needed.

At the level of individual counties, there are some familiar patterns. Galway dominates in terms of the share of housing completions in the region: accounting for 38% of the regional total in 2023, a experiencing a small dip to 35% in 2024 but with a rise to 40.5% in Q1 2025. This is both a reflection of and a contributor to Galway’s comparatively higher population growth over time. Between 1996 and 2022, Galway experienced by far the highest population growth rate in the region (47.1%) and now accounts for 31% of the region’s population (Census 2022). Clare has also shown steady growth in the last number of years, from 408 house completions in 2023 (12% of regional total) to 539 in 2024 (15% of regional total). As Table 3 illustrates, other counties have largely remained at similar levels and largely commensurate with their share of regional population; the next two sub-sections will give us a clearer picture of future patterns.

Table 3: New House Completions Western Region & State, 2023, 2024, Q1 2025.

Source: CSO New Dwelling Completions

Housing Commencements

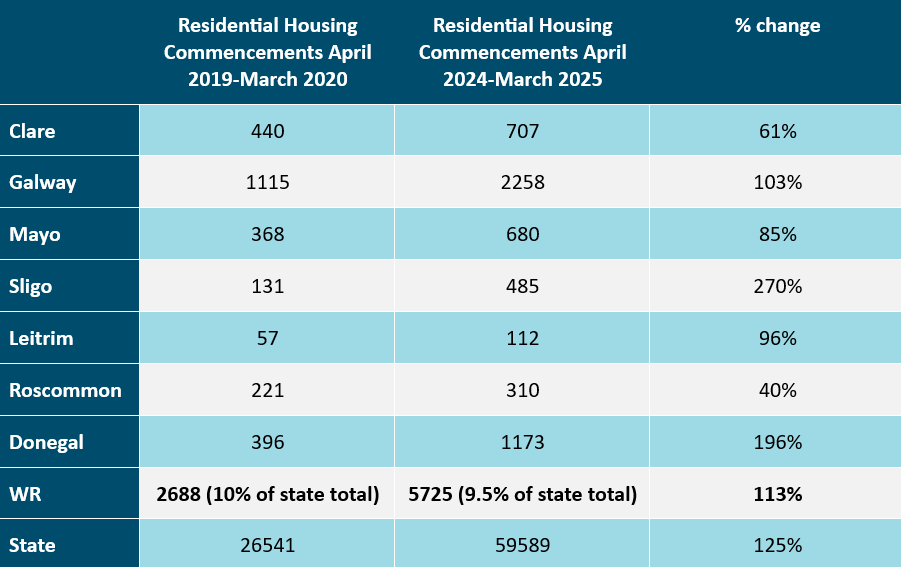

The figures on housing commencements presented in Table 4 provide us with some similar patterns to above and some interesting intra-regional variations. Overall, we can see that while the Western Region has experienced a really significant 113% increase in house commencements between April 2019-March 2020 and April 2024-March 2025, it is still under the percentage increase for the state overall of 125%. Housing commencements in the region remain a smaller percentage of the state total than might be expected or than is desirable from a regional development and growth perspective: the percentage has actually marginally declined in the last five years from 10% to 9.5%.

There are significant differences in the rate of growth between individual counties. Sligo experienced a massive 270% increase in housing commencements over the five-year period. However, this is from what was arguably a very low base of only 131 house commencements in the year April 2019-March 2020: its 8% of regional housing completions in the 2024/2025 period only brings it into line with what might be expected with its regional share of population. Donegal also experienced a very significant increase of over 196%, with 20% of the regional total of commencements in the 2024/2025 period, followed by Galway at 103%, which as was the case with housing completions, hovers around 40% of the regional total. Roscommon experienced the lowest growth, at only 40% over the five-year period. It also accounted for only just over 5% of the regional total in the 2024/2025 period, well below that of Sligo with a similar population base. Mayo also has a lower proportion than might be expected: 12% of the total but with 15% of the population base.

Table 4: Housing Commencements Western Region & State, Year to March 2020 and Year to March 2025.

Source: CSO New Dwelling Commencements.

Planning Permissions

Planning permission figures are a somewhat crude and imprecise measure of future housing availability because we cannot accurately predict how many planning permissions will ultimately result in completed new homes/apartments. However, we can discern some general patterns which are interesting to note.

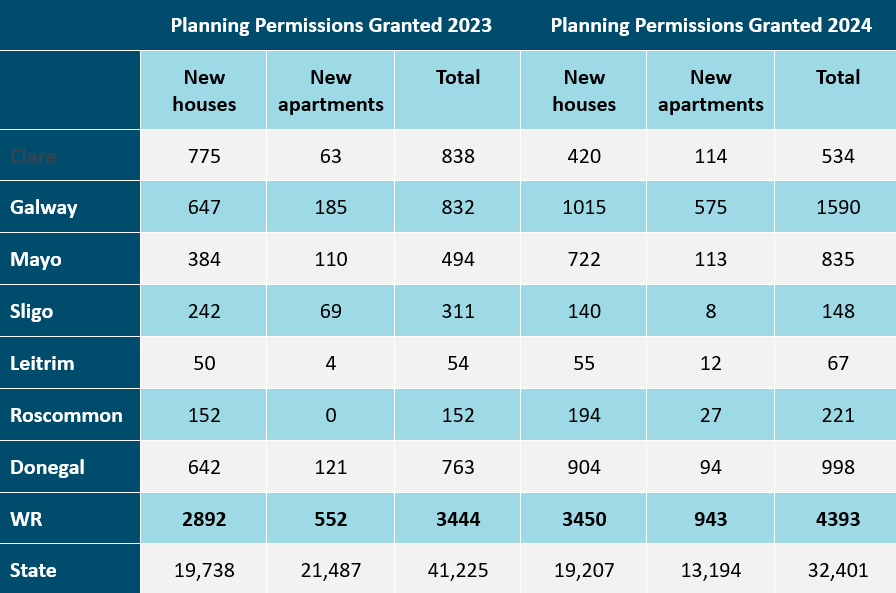

Perhaps the most positive recent development is a very significant 28% increase in the numbers of planning permissions granted in the Western Region from 2023 to 2024. The figures for the State overall actually declined by 21% in the same period, from 41,225 in 2023 to 32,401 in 2024. In line with this the Western Region counties accounted for 13.5% of planning permissions granted nationally in 2024, compared to 8% in 2023.

Galway again accounts for a high proportion of new planning permissions granted in the region in 2023 (24%) and especially so in 2024 (36%). Some fluctuations can be seen across most counties apart from Donegal which accounted for 22% of planning permissions granted in both years. Given Sligo’s position as a regional growth centre, the steep decline in planning permissions granted between 2023 and 2024 is particularly disappointing: It went from 311 planning permissions granted in 2023 (9% of the regional total) to only 148 in 2024 (3% of the regional total). A similar decline between 2023 and 2024 was experienced in Clare, albeit from a notably high starting point of 24% of regional planning permissions granted in 2023.

Table 5: Planning Permissions Granted, Western Region & State, 2023, 2024.

Source: CSO Planning Permissions Granted.

Conclusion

All of the key pillars of regional development – attracting investment and business growth, building third-level capacity, retaining and attracting talent, encouraging return and inward migration, encouraging tourism and the experience economy – are reliant to some degree on both the availability of suitable housing for rent or purchase and its being accessible at prices that are affordable relative to regional income levels. When we combine the above statistics on house completions and commencements with the increases in purchase and rental prices regionally, it is evident that there is need for a substantial increase in the supply of housing. While some of the statistics presented here in relation to completions and planning permissions suggest some movement in the right direction, this is not happening at the level that is needed either to meet current demand or provide for the kind of population growth and regional re-balancing which is desirable from a regional development perspective or which is envisaged within the National Planning Framework and the RSES of the Northern and Western and Southern Regions.

Taken alongside growing gaps in key regional indicators such as GVA and GDP, disposable income, investment in critical infrastructure, etc., the trend is towards continued and further over-development in the Eastern and Midland Region of the country in particular and under-development of the Northern and Western Region, of which the Western Region covered by WDC is a part. Without targeted interventions across multiple fronts, imbalances in terms of population growth across the regions are if anything likely to increase in the coming years with the Western Region’s share of national population decreasing further.

Download Visual Summary of Housing Stats for Western Region

[1] https://ww1.daft.ie/report/2024-Q4-rentalprice-daftreport.pdf?d_rd=1As

[2] https://www.gov.ie/en/department-of-housing-local-government-and-heritage/press-releases/government-to-introduce-major-reforms-to-the-rental-sector/

[3] Standardised average rent

[4] Standardised average rent