Last year I examined regional patterns in working from home, pre-Covid, see here.

It was clear that over the last few years, (2016-2019), up to the pandemic, there were differing regional patterns with higher rates in the Border, West and South-West, while Dublin had the lowest rate of those ‘usually working from home’.

In this insights blogpost, I examine the impact of Covid-19 and the Government’s work from home guidance on patterns of working from home by region, focusing on changes between 2019 and 2020.

Are there continuing regional differences and if so why and what might be the policy implications?

‘Usually’ Working from Home

The Central Statistics Office (CSO) Labour Force Survey (LFS) asks how often did you work from home in the last four weeks.If the response is that ‘At least half of the days worked at home’, then the response is categorised ‘as usually works from home’. If the response is ‘less than half the days worked but at least one hour’, then the response is categorised as sometimes working from home.

Those ‘sometimes working from home’ is discussed separately below.

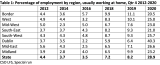

Table 1 below shows the percentage in employment by region[1] who report usually working from home, over the period since 2012.

The data is taken from the Q4 period (October to December). Therefore Q4 2019 is the period immediately preceding the pandemic, while Q4 2020 is one year on, during the pandemic. In Q4 2020, Level 4 and Level 5 restrictions applied, both of which advise working from home unless an essential service.

In the most recent LFS (Q4 2020), across the regions, all regions have more than one fifth of those employed usually working from home. Dublin has the highest incidence, with over two fifths – (40.3%), followed by Mid-East (26.6%), the South West (25.7%) and the West region (25%).

Those regions with the lower rates – though still all greater than one fifth – are the Midlands (23.2%), the Mid-West (23.0%), the South-East (21.0%) and the Border region (20.5%).

Trends – Pandemic related

Between 2019 and 2020 (Q4) there has been a 3.5 times increase nationally in the proportion of those in employment now ‘usually working from home’. Across the regions, the level of increase varies but all regions show at least a doubling of the rate of usually working from home pre and during the pandemic.

Those regions with a higher than average increase are the Mid-East (3.7 times increase) and Dublin with a six fold increase.

All other regions, while reporting a significant rate of increase is less than the national average, for example the West region shows a 2.5 times increase, and the rate in the Border region doubled.

Trends since 2012

In trying to understand factors influencing the level of working from home, it is worth looking at the trends pre-pandemic, which indicate the extent of working from home in the absence of any Government direction.

Table 1 shows that there is some evidence of a decline in the share of employed usually working from home between 2012 and 2016, with an increase evident across every region thereafter. This period coincides with a tighter labour market, with higher employment levels and low unemployment rates in 2019. This trend is also clear across every region, albeit with different levels in each (Table 1).

In a previous insights blogpost, I discussed the possible relationship between working from home and employment and unemployment levels.

In the couple of years preceding the pandemic (2016-2019) the Dublin region had some of the lowest rates, whereas the more rural regions, such as the Border and West regions have some of the higher rates of those usually working from home.

‘Sometimes’ Working from Home

The other measure of those working from home is those ‘sometimes working from home’ categorised as those who have worked for at least one hour from home in the last four weeks. It is clear that there is a different regional pattern for the categories of usually and sometimes working from home.

In 2019, the national average for those sometimes working from home was 13.3%, with Dublin, the Mid-East and West regions having higher than average rates (Table 2).

In 2020, the national average was 8.3%, with the Mid-East 9.7%, South-East 9.7%, Midlands 9.1% and South-West 8.6% – the regions with higher-than-average rates. The regions now with rates slightly below the average are Dublin 7.6%, the Mid-West 6.8% and the Border region 6.7%.

Comparing pre-pandemic levels in 2019 with a year later in the midst of the pandemic it is clear that the incidence of those sometimes working from home is down in every region except the Border (and just a slight decline in the Midlands). It is likely that some of those who previously ‘sometimes’ worked from home are now ‘usually’ working from home, arising from the Government public health measures.

For example, looking at the Dublin region, considering the six-fold increase in those ‘usually’ working from home between 2019 and 2020, it is probable that most of the decline in those ‘sometimes’ working from home in Dublin between 2019 and 2020 are now ‘usually’ working from home in 2020.

Trends since 2012

In trying to understand the changing patterns in usually and sometimes working from home, it is useful to look at patterns preceding the pandemic.

Nationally, the rate of those in employment ‘sometimes’ working from home has been decreasing from 2012 to 2016 with levels increasing from then to 2019. In the couple of years pre-pandemic (2016-2019), the lowest rates of those ‘sometimes’ working from home are in the Border and Midland regions, while Dublin, West, Mid-East and Mid-West regions had higher rates.

What are the factors that have influenced the extent of working from home and the patterns of whether the practice is ‘sometimes’ or ‘usually’. It is clear that Government guidance on working from home during the pandemic has been the reason for the significant increase in those ‘usually’ working from home.

How can the regional differences be explained?

Regional Difference: Explanations and Policy Insights

It is likely regional differences are due to a combination of factors including;

- Self-employment

- Occupational profile and the extent of working from home potential

- Commuting

- Opportunity

- Self-employment

It is worth noting the measure of employment that is used. The LFS data examined here refers to all those in employment, both self-employed and employees[2].

The self-employed include many who usually work from home for example home-based sole traders and self-employed such as GPs, childminders and those engaged in various skilled trades.

In the context of regional difference it is clear that some regions have a higher level of self-employment and it is likely that some have a higher incidence of home working.

There are relatively high rates of self-employment in more rural areas, examined in a previous insights blogpost, showing the most rural counties with higher than average rates (15.6%).

For example, five of the Western Region counties are in the top ten nationally in terms of share of self-employment, Leitrim (20.3%), Roscommon (19.9%), Mayo (19.6%), Galway county (19.5%) and Clare (19.5%) all having close to 1 in 5 of their workers self-employed.

- Occupational and sectoral profile of the region

The occupational and sectoral profile of regions can also influence the ‘working from home potential’.

It is clear that some occupations have greater working from home potential, e.g. those engaged in administrative and business roles. Similarly, some sectors will have a greater incidence of working from home such as roles within the ICT sector. Working from home has been an established practice within some companies for decades (e.g. Cisco, see here for more detail).

As Table 1 shows, those regions with the highest rates of ‘usually working from home’ are those regions with the largest urban centres and their labour catchments, hosting many occupations and industries with greater working from home potential; Dublin and the Mid-East region, Cork (South-West region) and Galway (West region).

Those regions with a higher exposure to both occupations and sectors with more limited working from home potential, for example the tourism sector and accommodation and hospitality roles are also those most impacted by the Government restrictions, as a means to enforce social distancing[3]. It is these regions who have seen the rate of ‘usually work from home’ increase at a lower rate.

Previous insights blog posts have examined the potential sectoral impact of Covid-19 on the Western Region. Three broad sectors, ‘Accommodation and Food’ Services, ‘Wholesale and Retail’ and ‘Construction’ have been hit the hardest, see insights blogpost here and these are relatively more highly concentrated in more rural regions including the Western Region.

- Commuting

Pre Covid-19, the most often cited factor influencing the demand to work from home has been commuting. This was noted in the Government report Remote Work In Ireland, 2019.

As noted, the spatial pattern evident in Table 1 highlights the influence of the larger commuting catchments. It is also clear from survey evidence that reduced commuting is a key factor supporting a demand for more working from home.

Both national surveys of Remote Working conducted by WDC-NUIG, (over 12,000 responses) in 2020, identified the top advantage of working from home being ‘no traffic and no commute’ cited by over three quarters in each survey.

In both surveys most respondents wanted to continue to work from home post Covid. In Phase I, 83% wanted to continue to work remotely, while in Phase II 94% report wanting to continue remote working. While the survey evidence does not generally discriminate between journey time or distance is it very likely that the greater the journey time/distance the more it is a factor.

The most recent Census data (2016) notes that commuting times have been increasing and commuters in counties bordering Dublin had the longest average commuting time. It is likely that it is in the commuter belts of the urban catchments where the greatest incidence in working from home is occurring.

- Opportunity

Pre-Covid-19, a key determinant of whether one could work from home (as an employee) was with the agreement of the employer. This required a complementary mix of both role suitability and an employer supportive of the practice.

This is likely to have impacted the rate of usually and sometimes working from home and could partly explain the dramatic increase in ‘usually working from home’ in the Dublin region since the pandemic, in contrast to the relatively low rates before.

Similarly, the consistent increasing trend in ‘sometimes working from home’ in the Dublin region pre-pandemic (2012-2019), suggests concessions on the part of some employers in the context of an ever tightening labour market.

The pandemic has forced many (employers and employees) to challenge the view that many roles may not be suitable, and that work cannot be performed as successfully from home.

The experience of employers since the pandemic has been documented see here and illustrates both a changed perception of the practice but also a cohort who remain resistant to working from home in the absence of Government guidelines. Large employers are based in larger urban centres, once more influencing the spatial pattern of those usually working from home. The incidence of these roles are much greater in the Dublin region this can help explain the very significant increase in those usually working from home in the Dublin region.

Covid-19, Working from Home and some Policy Insights

The following are some policy implications arising from the changed levels and patterns of working from home, arising from Covid -19 and Government guidelines.

- Those regions with higher rates of working from home are likely to be able to sustain employment especially in the context of further Covid related restrictions.

- In the context of sustaining employment, at a regional level it is clear that Dublin and to a lesser extent the other larger urban centres will be less exposed to the detrimental impacts of Covid.

- The ability to work from home is concentrated among professional occupations. Those regions with a greater concentration of these occupations are likely to be less adversely impacted.

- The inability to work from home will impact on those occupations and industries and will likely involve job losses, impacting more severely those regions with higher exposure to those sectors (Tourism, accommodation, hospitality). Many of the these are in rural towns in the West and Border regions with potentially detrimental long term effects.

- Commuting will influence the demand for continued home working. It is likely that it is in the commuter belts of the urban catchments where the greatest levels of working from home is occurring. It is also likely that this is where the greatest levels of working from home will continue post the pandemic.

- Post pandemic we are likely to see a greater incidence of working from home than pre-pandemic, though this is likely to change from the current ‘usually’ practice to a ‘sometimes’ practice.

What will the patterns be when we emerge from the pandemic? The WDC will continue to monitor trends and highlight issues as they emerge. It is intended to undertake another National Survey in conjunction with NUI Galway in April/May 2021 following up on the original see here, examining the employee perspective on working from home and one year on from the start of the pandemic.

The views expressed here are those of the author and do not necessarily represent or reflect the views of the WDC.

Deirdre Frost

[1] The regions are composed of counties as follows. Border: Donegal, Sligo, Leitrim, Cavan, Monaghan. West: Galway, Mayo, Roscommon. Mid-west: Clare, Tipperary, Limerick. South East: Waterford, Kilkenny, Carlow, Wexford. South-West: Cork, Kerry. Dublin. Mid-East: Wicklow, Kildare, Meath, Louth. Midlands: Longford, Westmeath, Offaly, Laois.

[2] The ESRI note that pre pandemic, 13.8% of employees nationally work from home (both usually and sometimes). Here, the data indicates that in 2019 about one fifth or 21.5% work from home (combining Tables 1 & 2). The difference between the ESRI and WDC figures (of about 7% points) is accounted for by the inclusion of the self-employed in the WDC data. https://www.esri.ie/system/files/publications/SUSTAT87.pdf

[3] See also Covid-19, Occupational Social Distancing and Remote Working Potential in Ireland COVID19_FC_JD_2020_website.pdf (ucc.ie)